Investment Opportunities

Storage

Storage Outlook

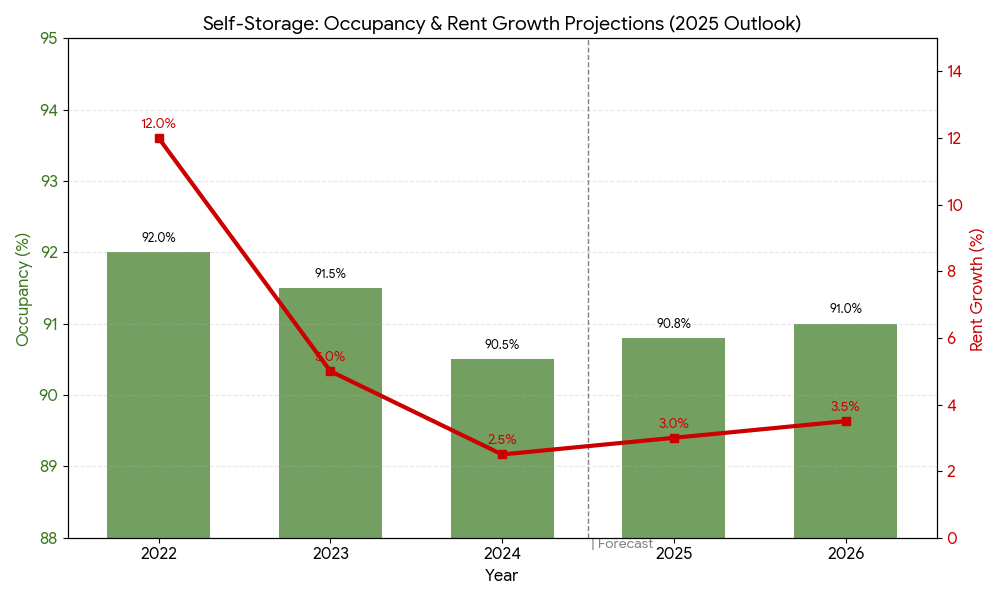

Figure 1: Storage Occupancy (bar) and Rent Growth (line) by year, with forecasts. National occupancy has stabilized above pre-pandemic levels (projected near 90–91%). Rent growth is positive but moderate, expected in the 1.5–3.5% range as the market balances supply.

Resilient Fundamentals: Supply Constraints & Stabilization

The Self-Storage sector is transitioning from the hyper-growth phase of the pandemic era into a period of stabilization and selectivity in 2025. National occupancy, while slightly off its 2021 peak, remains robust, hovering around 90–91% for same-store facilities. This resilience is largely attributed to a significant slowdown in new supply. Rising interest rates and high construction costs throughout 2024 caused many planned projects to be shelved, leading to a national under-construction pipeline contraction to approximately 2.6% of existing inventory. This easing of new competition provides existing, well-located facilities with greater pricing power and is a key driver for the positive outlook.

Demand Drivers: The “Four Ds” and Urban Density

Demand for self-storage is fundamentally non-discretionary and driven by the “Four Ds”: Death, Divorce, Downsizing, and Dislocation (moving/job changes). While high mortgage rates have suppressed moving-related demand (which historically accounts for about 50% of storage customers), this is being offset by:

Downsizing: Economic uncertainty and high housing costs are driving more people to downsize into smaller homes or apartments, necessitating external storage.

Commercial Use: E-commerce sellers, remote workers, and tradespeople use units for inventory and equipment, supporting the commercial segment.

Urban Densification: As living spaces in high-cost metro areas shrink, offsite storage becomes essential.

The market size is estimated to be valued at $61.00 billion in 2025, growing at a solid CAGR of 5.6% through 2032. This underlying demand ensures the sector’s reputation as a recession-resilient asset class.

Spotlight on Segments: Climate Control and Location

Performance is now heavily stratified by asset quality and location.

Climate-Controlled (CC) Units are performing better than non-climate-controlled (NCC) units, with CC units seeing year-over-year rate increases of around 1.3% compared to flat or slightly negative growth for NCC units in some markets. This highlights the “flight to quality” among consumers.

Supply-Constrained Markets are significantly outperforming. Coastal and high-barrier-to-entry metros like Manhattan, Chicago, and Minneapolis, where new development is severely limited, are seeing solid rent growth. Conversely, Sun Belt metros like Charlotte and Phoenix, which were heavily overbuilt in recent years, still face temporary supply pressure and rate compression.

CMIC’s investment strategy favors high-quality assets in these supply-constrained markets, focusing on the spread between the new tenant (street) rate and the existing tenant (contract) rate, which has widened to as much as 48% for some operators.

Outlook: Stability and Selective Growth

Overall, self-storage offers stable cash flows and a defense against market volatility, underpinned by low operating costs (typically 30–40% of revenue). While overall rent growth has been moderate, sequential monthly growth is trending positive, signaling stabilization. Investors should focus on assets with high existing occupancy (above 90%) and those that benefit from the decline in new construction. For CMIC, self-storage remains a strategic allocation that provides portfolio diversification and a strong hedge against economic uncertainty, provided that underwriting is disciplined and focused on micro-market supply analysis.